Instantly Calculate Your Pay Check — Fast, Accurate, Free to Access

Free, accurate paycheck calculations for all 50 states. Understand your taxes, plan your budget, and take control of your finances.

- SSL Secured

- IRS Compliant

500+

Calculations Done

States Covered

99%

Accuracy Rate

4.9

Star Ratings

How It Works

Get your paycheck estimate in three simple steps

Select Your State

Choose your state to apply the correct state income tax rates and local deductions.

Enter Your Salary

Input your gross annual salary or hourly rate along with your pay frequency.

See Breakdown Results

Instantly view your take-home pay with a complete breakdown of all deductions.

Benefits of Choosing Us

Built by financial experts, trusted by millions. Our calculators are designed to give you accurate, reliable results every time.

Pay Period Dates

The specific period employees are being paid for (usually bi-weekly or monthly ). Helps track earnings and ensure correct compensation.

Earnings

Details your total wages, salaries, bonuses, etc., for the pay period. It helps with transparency, budgeting, and tax reporting.

Net Pay

The take-home pay after deductions (taxes, benefits, etc.) are subtracted from gross pay (total earnings). It's crucial for budgeting and tax purposes.

Taxes Withheld

Federal, state, and local income taxes deducted from employee's paycheck. Ensures you pay the right amount throughout the year.

Contributions

Employer's share of employee's benefits package (retirement, health insurance, etc.). Significantly impacts their financial well-being.

Deductions

Money withheld from gross pay for taxes, benefits, garnishments, etc. It ensures compliance, transparency, and accurate budgeting.

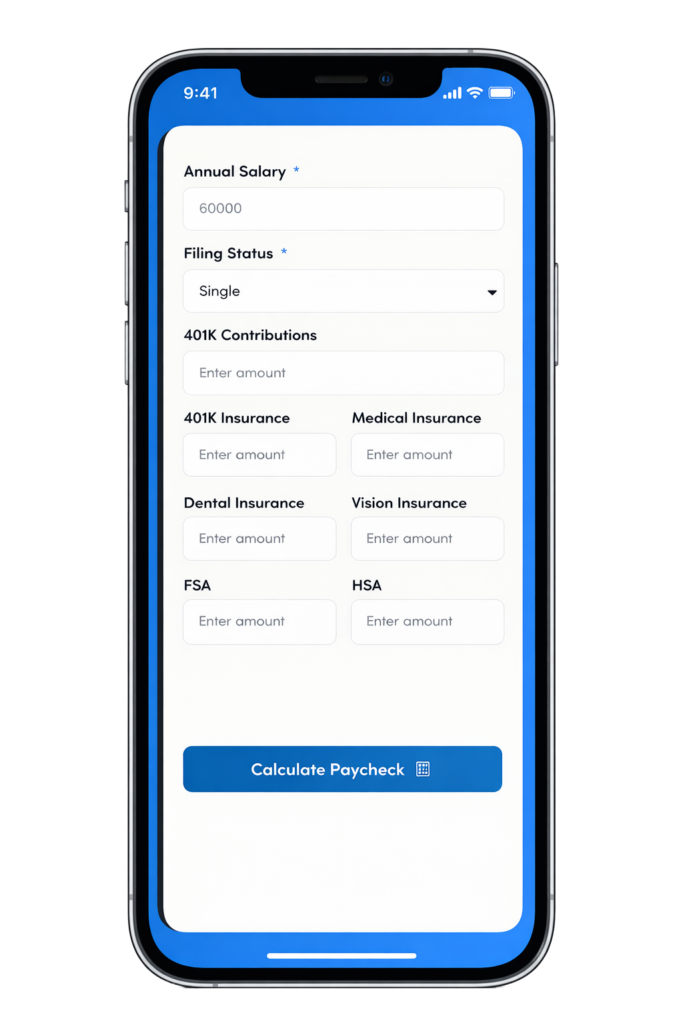

Paycheck Calculator: Calculate Your Take-Home Pay

A paycheck calculator estimates your take-home pay by factoring in federal taxes, state taxes, Federal Insurance Contributions Act (FICA) taxes, and deductions from your gross pay. Enter your salary or hourly wage, pay frequency, filing status, and deduction details to get an accurate picture of your net pay every pay period.

Understanding Your Paycheck

What is Gross Pay and Net Pay?

Gross pay is your total earnings before any taxes or deductions are withheld. Net pay—also called take-home pay—is what remains after federal income tax, state income tax, FICA taxes, and voluntary deductions are subtracted. The formula is:

Gross Pay − Taxes − Deductions = Net Pay

In the U.S., gross pay is the figure used on mortgage applications, tax brackets, and salary comparisons. Net pay is the figure that hits your bank account and funds your actual expenses.

Pay Frequency

Pay frequency refers to how often your employer issues paychecks. There are 8 common pay frequency options used by U.S. employers:

| Pay Frequency | Description |

|---|---|

| Daily | Paid every working day. Uncommon for salaried positions. |

| Weekly | Paid each week, typically on the same day each pay period. |

| Bi-weekly | Paid every other week, generating 26 paychecks per year. |

| Semi-monthly | Paid twice per month on set dates (usually the 15th and 30th), generating 24 paychecks per year. |

| Monthly | Paid once per month, generating 12 paychecks per year. |

| Quarterly | Paid 4 times per year. Uncommon. |

| Semi-annually | Paid 2 times per year. Uncommon. |

| Annually | Paid once per year. Uncommon. |

How is Pay Frequency Used to Calculate Payroll?

Pay frequency has no effect on annual tax liability. It only affects the size of each individual paycheck. For salaried employees, the number of pay periods in a year determines gross pay per paycheck. For example, a salaried employee earning $52,000 per year receives:

$1,000 per paycheck on a weekly schedule (52 pay periods)

$2,166.67 per paycheck on a semi-monthly schedule (24 pay periods)

Bi-weekly vs. Semi-monthly

Bi-weekly pay generates 26 paychecks per year (27 in a leap year), while semi-monthly pay generates exactly 24. Both frequencies result in 2 paychecks per month for most months, but bi-weekly employees receive 3 paychecks in 2 months out of the year. Semi-monthly pay always lands on set calendar dates, while bi-weekly pay shifts based on the day of the week.

Federal Taxes: An Overview

When your employer calculates your take-home pay, federal taxes are the largest withholdings from each paycheck. There are 3 main categories of federal tax withholding: income tax, FICA (Federal Insurance Contributions Act) tax, and Federal Unemployment Tax Act (FUTA) tax.

Federal Paycheck Quick Facts:

Federal income tax rates range from 10% to 37% depending on taxable income.

The U.S. median household income (adjusted for inflation) in 2024 was $83,730.

9 U.S. states impose no state income tax for tax years 2025 and 2026.

Income Tax

How Your Paycheck Works: Income Tax Withholding

Federal income tax withholding is the portion of each paycheck sent directly to the Internal Revenue Service (IRS) to cover your annual income tax liability. The federal government collects income tax gradually throughout the year by deducting it from each paycheck, rather than requiring a lump-sum payment at year-end.

Your employer calculates the withholding amount based on the information you provide on your Form W-4 (Employee’s Withholding Certificate). Submit a W-4 when you start a new job, and resubmit one after any major life change, such as marriage, divorce, or the birth of a child.

Calculating weekly take-home pay is not as simple as multiplying your hourly wage by hours worked or dividing your annual salary by 52. Federal income tax, FICA taxes, state taxes, and benefit deductions all reduce the gross amount before you receive your paycheck. That is where a paycheck calculator becomes essential.

How is Federal Withholding (Federal Income Tax) Calculated?

Federal income tax is calculated based on your taxable income, filing status, and the information provided on your W-4, using the tax tables in IRS Publication 15-T. The process follows 4 steps:

1. Determine gross pay—total earnings for the pay period, including wages, bonuses, overtime, and commissions.

2. Subtract pre-tax deductions—contributions to a 401(k), health insurance premiums, and Health Savings Account (HSA) contributions reduce your taxable income.

3. Calculate taxable income—gross pay minus pre-tax deductions equals taxable income.

4. Apply the federal tax brackets—taxable income is divided across progressive rate brackets (10%, 12%, 22%, 24%, 32%, 35%, and 37%).

The higher your taxable income, the higher the marginal rate applied to each additional dollar earned above each bracket threshold.

Withholding Requirements

Exemptions from Federal Taxes

You are exempt from federal income tax withholding if you meet both of the following 2 conditions:

1. In the prior tax year, you received a full refund of all federal income tax withheld because your tax liability was zero.

2. In the current tax year, you expect to owe zero federal income tax and expect a full refund of all withheld amounts.

Exemption eligibility is typically tied to income falling below the standard deduction threshold. For 2026, those thresholds are:

$16,100 for single filers or married filing separately

$32,200 for married filing jointly

$24,150 for head of household

Claim exempt status by indicating it on your W-4. Claiming exempt when ineligible can result in a large tax bill and potential penalties at filing.

Single vs. Head of Household

Head of Household filers are taxed at lower effective rates than Single filers because the Head of Household tax brackets are wider. To qualify as head of household, you must be unmarried and have paid more than half the cost of maintaining a home for yourself and a qualifying dependent.

Choosing the wrong filing status costs money and time. Single filers who qualify as head of household leave money on the table by filing as single. Verify all eligibility conditions before selecting a filing status on your W-4.

W-4 Form: What it is and Why it's Important

The W-4 form (Employee’s Withholding Certificate) determines the amount of federal income tax withheld from each paycheck. Completing it accurately keeps your withholding aligned with your actual tax liability, reducing the chance of owing a large balance or receiving an unexpectedly large refund at tax time.

The current W-4 follows a 5-step process covering:

1. Personal information and certification

2. Multiple jobs or spouse employment

3. Dependents and qualifying credits

4. Other income adjustments (non-wage income, additional deductions)

5. Additional withholding per pay period

Updates to the Federal W-4 in 2020

In 2020, the IRS redesigned the W-4 form to eliminate withholding allowances entirely. The prior W-4 (2019 and earlier) used a number-of-allowances system. The updated form replaced allowances with dollar amounts for greater accuracy. Key changes include:

Step 2—Check the box if you hold multiple jobs or your spouse also works.

Step 3—Enter a dollar amount for dependents. Multiply children under 17 by $2,000 and other dependents by $500, then add the total. (Applies to total income of $200,000 or less, or $400,000 for married filers.)

Step 4a—Enter non-wage income (dividends, interest) not subject to automatic withholding.

Step 4b—Enter any additional withholding amount per pay period.

Employees currently on the old format are not required to update their W-4. Update the form using the current version when any change in circumstances—new job, marriage, or change in dependents—makes it necessary.

FICA Tax

How Your Paycheck Works: FICA Withholding

FICA (Federal Insurance Contributions Act) withholding funds 2 federal programs: Social Security and Medicare. Both employees and employers share FICA contributions equally. For employees, FICA is automatically deducted from each paycheck. For self-employed individuals, the full FICA amount (15.3%) applies as the self-employment tax, though half is deductible when filing taxes.

What is FICA on My Paycheck?

FICA on your paycheck is the combined deduction for Social Security tax and Medicare tax. These deductions fund retirement benefits, disability benefits, and health insurance for seniors. FICA taxes are mandatory for nearly all U.S. wage earners—there is no exemption based on income level for Medicare, and Social Security withholding applies up to an annual wage cap.

Social Security and Medicare Taxes: How Much?

| Tax | Employee Rate | Employer Rate | Wage Cap |

|---|---|---|---|

| Social Security (2025) | 6.2% | 6.2% | $176,100 |

| Social Security (2026) | 6.2% | 6.2% | $184,500 |

| Medicare | 1.45% | 1.45% | No limit |

| Additional Medicare Tax | 0.9% | Not applicable | See thresholds below |

The Additional Medicare Tax of 0.9% applies to wages above the following thresholds (employee-only, not matched by employer):

| Filing Status | Threshold |

|---|---|

| Single / Head of Household | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

Federal Unemployment Tax Act (FUTA)

The Federal Unemployment Tax Act (FUTA) is a payroll tax paid exclusively by employers, not employees. FUTA funds state unemployment insurance programs. The standard FUTA rate is 6% on the first $7,000 of each employee’s wages per year. Employers who pay state unemployment taxes on time receive a tentative credit of 5.4%, reducing the effective FUTA rate to 0.6% for most employers.

FUTA does not appear as a deduction on employee paychecks because employees bear no FUTA liability.

State and Local Taxes

Local Factors Affecting Your Paycheck

State and local income taxes reduce take-home pay beyond federal withholdings, and the impact varies significantly by location. There are 3 categories of state income tax structures in the U.S.:

1. Progressive tax states (26 states)—Tax rates increase as income rises. California has the highest top marginal state income tax rate at 13.30%.

2. Flat tax states (15 states)—A single rate applies to all income levels. These states are Arizona, Colorado, Georgia, Idaho, Illinois, Iowa, Indiana, Ohio, Michigan, Mississippi, Kentucky, Louisiana, North Carolina, Pennsylvania, and Utah.

3. No-income-tax states (9 states)—Alaska, Florida, Nevada, New Hampshire, South Dakota, Texas, Tennessee, Washington, and Wyoming—impose no state income tax.

Tennessee and New Hampshire do not tax wages or salaries, but they do tax interest and dividend income. Most U.S. cities and counties do not impose a local income tax, but those that do—including New York City—can significantly affect take-home pay for approximately 10% of the U.S. population.

Paycheck Calculators by State

Take-home pay calculations differ by state because tax rates, brackets, and withholding rules vary. Use state-specific paycheck calculators to account for your exact state tax rate, any applicable local taxes, state unemployment insurance, and state-specific deductions such as short-term disability or paid family leave programs. Enter your work state (not your residence state) to apply the correct withholding rates.

Deductions and Withholdings

How Your Paycheck Works: Deductions

Deductions reduce the amount of your gross pay that is subject to taxation, lowering your tax liability and your take-home pay simultaneously. Common paycheck deductions include employer-sponsored health insurance premiums, 401(k) or 403(b) retirement contributions, HSA or Flexible Spending Account (FSA) contributions, and wage garnishments ordered by a court.

Deduction vs. Withholding

A withholding is a mandatory tax payment taken directly from your paycheck by your employer on behalf of the government. A deduction is a reduction in taxable income from a qualifying expense or contribution. Withholdings include federal income tax, state income tax, and FICA taxes. Deductions include retirement contributions, health insurance premiums, and HSA contributions. Both reduce your net pay, but deductions also reduce the taxable income base on which withholdings are calculated.

Pre-tax and Post-tax Deductions

There are 2 types of paycheck deductions:

Pre-tax deductions are subtracted from gross pay before federal and state income taxes are calculated. Pre-tax deductions lower your taxable income and reduce your total tax bill. Examples include 401(k) contributions, HSA contributions, FSA contributions, and employer-sponsored health insurance premiums. Electing to save 10% of income into a 401(k) means that 10% is deducted before taxes, shrinking your taxable income by that amount.

Post-tax deductions are subtracted from pay after income taxes have been applied. The money has already been taxed, but future withdrawals may be tax-free. The most common post-tax deduction is a Roth 401(k) contribution. Roth accounts are advantageous for workers early in their careers or those who expect to be in a higher tax bracket in retirement.

Are Some Deductions Not Taxed by Federal Income Tax?

Yes, several pre-tax deductions are exempt from federal income tax. The 3 most common examples are:

1. 401(k) and 403(b) contributions—Traditional retirement contributions reduce federal taxable income in the year they are made.

2. Health insurance premiums—Employer-sponsored health insurance premium contributions deducted pre-tax are not included in taxable wages.

3. Flexible Spending Accounts (FSA) and Health Savings Accounts (HSA)—Pre-tax contributions to these accounts for qualified medical expenses are excluded from taxable income.

Post-tax deductions like Roth 401(k) contributions do not reduce current taxable income, but qualified withdrawals in retirement are tax-free.

Tax Brackets

2026 Tax Brackets (due April 2027)

The 2026 federal income tax brackets apply to income earned in tax year 2026, with returns due in April 2027. The standard deduction for 2026 is $16,100 for single filers, $32,200 for married filing jointly, and $24,150 for head of household.

Single Filers

| Taxable Income | Rate |

|---|---|

| $0 – $12,400 | 10% |

| $12,400 – $50,400 | 12% |

| $50,400 – $105,700 | 22% |

| $105,700 – $201,775 | 24% |

| $201,775 – $256,225 | 32% |

| $256,225 – $640,600 | 35% |

| $640,600+ | 37% |

Married Filing Jointly

| Taxable Income | Rate |

|---|---|

| $0 – $24,800 | 10% |

| $24,800 – $100,800 | 12% |

| $100,800 – $211,400 | 22% |

| $211,400 – $403,550 | 24% |

| $403,550 – $512,450 | 32% |

| $512,450 – $768,700 | 35% |

| $768,700+ | 37% |

Married Filing Separately

| Taxable Income | Rate |

|---|---|

| $0 – $12,400 | 10% |

| $12,400 – $50,400 | 12% |

| $50,400 – $105,700 | 22% |

| $105,700 – $201,775 | 24% |

| $201,775 – $256,225 | 32% |

| $256,225 – $384,350 | 35% |

| $384,350+ | 37% |

Head of Household

| Taxable Income | Rate |

|---|---|

| $0 – $17,700 | 10% |

| $17,700 – $67,450 | 12% |

| $67,450 – $105,700 | 22% |

| $105,700 – $201,775 | 24% |

| $201,775 – $256,200 | 32% |

| $256,200 – $640,600 | 35% |

| $640,600+ | 37% |

The 2026 federal income tax brackets apply to income earned in tax year 2026, with returns due in April 2027. The standard deduction for 2026 is $16,100 for single filers, $32,200 for married filing jointly, and $24,150 for head of household.

| Tax Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | $0- 12,400 | $0-24,800 | $0-17,700 |

| 12% | $12,401-50,400 | $24,801-100,800 | $17,701-67,450 |

| 22% | $50,401-105,700 | $100,801-211,400 | $67,451-105,700 |

| 24% | $105,701-201,775 | $211,401-403,550 | $105,701-201,775 |

| 32% | $201,776-256,225 | $403,551-512,450 | $201,776-256,200 |

| 35% | $256,226-640,600 | $512,451-768,700 | $256,201-640,600 |

| 37% | $640,601 or more | $768,701 or more | $640,601 or more |

2025 Tax Brackets (due April 2026)

The 2025 federal income tax brackets apply to income earned in tax year 2025, with returns due in April 2026. The standard deduction for 2025 is $15,750 for single filers,$31,500 for married filing jointly, and $23,625 for head of household.

Single Filers

| Taxable Income | Rate |

|---|---|

| $0 – $11,925 | 10% |

| $11,925 – $48,475 | 12% |

| $48,475 – $103,350 | 22% |

| $103,350 – $197,300 | 24% |

| $197,300 – $250,525 | 32% |

| $250,525 – $626,350 | 35% |

| $626,350+ | 37% |

Married Filing Jointly

| Taxable Income | Rate |

|---|---|

| $0 – $23,850 | 10% |

| $23,850 – $96,950 | 12% |

| $96,950 – $206,700 | 22% |

| $206,700 – $394,600 | 24% |

| $394,600 – $501,050 | 32% |

| $501,050 – $751,600 | 35% |

| $751,600+ | 37% |

Married Filing Separately

| Taxable Income | Rate |

|---|---|

| $0 – $11,925 | 10% |

| $11,925 – $48,475 | 12% |

| $48,475 – $103,350 | 22% |

| $103,350 – $197,300 | 24% |

| $197,300 – $250,525 | 32% |

| $250,525 – $375,800 | 35% |

| $375,800+ | 37% |

Head of Household

| Taxable Income | Rate |

|---|---|

| $0 – $17,000 | 10% |

| $17,000 – $64,850 | 12% |

| $64,850 – $103,350 | 22% |

| $103,350 – $197,300 | 24% |

| $197,300 – $250,500 | 32% |

| $250,500 – $626,350 | 35% |

| $626,350+ | 37% |

The 2025 federal income tax brackets apply to income earned in tax year 2025, with returns due in April 2026. The standard deduction for 2025 is $15,750 for single filers,$31,500 for married filing jointly, and $23,625 for head of household.

| Tax Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | $0 – 11,925 | $0 – 23,850 | $0 – 17,000 |

| 12% | $11,925 – 48,475 | $23,850 – 96,950 | $17,000 – 64,850 |

| 22% | $48,475 – 103,350 | $96,950 – 206,700 | $64,850 – 103,350 |

| 24% | $103,350 – 197,300 | $206,700 – 394,600 | $103,350 – 197,300 |

| 32% | $197,300 – 250,525 | $394,600 – 501,050 | $197,300 – 250,500 |

| 35% | $250,525 – 626,350 | $501,050 – 751,600 | $250,500 – 626,350 |

| 37% | $626,350+ | $751,600+ | $626,350+ |

Calculating Your Paycheck

What's a Salary Paycheck Calculator?

A salary paycheck calculator is a free online tool that estimates your net pay (take-home pay) by applying federal taxes, state taxes, FICA withholdings, and voluntary deductions to your gross annual salary or hourly wage. Enter your salary or pay rate, select your state and pay frequency, and input your W-4 information and deductions, and the calculator outputs your estimated paycheck amount for that pay period.

Salary paycheck calculators are useful for employees reviewing a new job offer, workers evaluating the impact of a raise, and employers verifying payroll accuracy before issuing paychecks.

How Do I Calculate My Paycheck Taxes?

To calculate paycheck taxes manually, follow these 8 steps:

1. Identify all income sources—wages, bonuses, commissions, overtime, and any other earnings for the pay period.

2. Calculate gross pay—total all earnings before deductions or taxes.

3. Subtract pre-tax deductions—remove 401(k) contributions, health insurance premiums, and HSA or FSA contributions from gross pay.

4. Calculate taxable income—gross pay minus pre-tax deductions equals taxable income.

5. Apply federal income tax brackets—use IRS Publication 15-T tax tables and the employee’s W-4 filing status to determine federal income tax withholding.

6. Calculate FICA taxes—withhold 6.2% for Social Security (up to the annual wage cap) and 1.45% for Medicare.

7. Apply state and local income taxes—use the applicable state tax rate and any local tax rate for the employee’s work location.

8. Subtract post-tax deductions—remove Roth 401(k) contributions, wage garnishments, or other post-tax deductions.

The result is net pay.

Gross Pay Method

The gross pay method refers to whether gross pay is entered as an annual amount or a per-period amount. There are 2 ways to input gross pay in a paycheck calculator:

Annual amount—your total salary for the full year (e.g., $52,000). The calculator divides this by the number of pay periods to determine per-period gross pay.

Per-period amount—the gross pay for a single pay period (e.g., $1,000 per week for a $52,000 annual salary paid weekly).

Both methods produce the same result. Use the annual amount when comparing offers or planning annual budgets. Use the per-period amount when calculating a specific paycheck.

Bonuses and Taxes

Increasing Your Take-Home Pay

How Can I Reduce My Taxes?

There are 6 practical strategies to legally reduce taxes and increase take-home pay:

1. Maximize pre-tax retirement contributions—Contributing more to a traditional 401(k) or 403(b) reduces taxable income directly. For 2025, the 401(k) employee contribution limit is $23,500 ($31,000 for workers aged 50 and older).

2. Use a Flexible Spending Account (FSA) or Health Savings Account (HSA)—FSA and HSA contributions are pre-tax, reducing taxable income while covering qualified medical expenses. These are dollar-for-dollar reductions to taxable income.

3. Review and update your W-4—Adjusting withholding allowances, claiming dependents accurately, or accounting for deductions on your W-4 prevents over-withholding and increases each paycheck.

4. Claim all eligible tax deductions and credits—tax deductions lower taxable income. Tax credits directly reduce your tax bill. Common deductions include student loan interest, qualified education expenses, and IRA contributions not covered through payroll.

5. Reevaluate benefit deductions—Enrolling in employer-sponsored benefits such as dependent care FSAs, commuter benefits, or additional voluntary insurance plans funded pre-tax reduces taxable income.

6. Work overtime strategically—Non-exempt employees covered by the Fair Labor Standards Act (FLSA) earn at least 1.5 times their regular hourly rate for hours worked over 40 in a workweek. Overtime increases gross earnings, which increases net pay despite higher marginal withholding.

The One Big Beautiful Bill Act

The One Big Beautiful Bill (enacted in 2025) introduced 4 temporary deductions available for tax years 2025 through 2028:

Qualified tips—Up to $25,000 per year in qualified tips may be deducted (phases out above $150,000 modified adjusted gross income, or $300,000 for joint filers).

Overtime compensation—Up to $12,500 per year for single filers, or $25,000 for joint filers, in qualified overtime pay may be deducted (phases out above $150,000, or $300,000 for joint filers).

Car loan interest—Up to $10,000 per year in interest paid on a loan for a qualified vehicle purchase may be deducted (phases out above $100,000, or $200,000 for joint filers).

Senior deduction—Individuals aged 65 and older may claim an additional $6,000 per year ($12,000 for qualifying married couples) (phases out above $75,000, or $150,000 for joint filers).

These deductions do not require choosing between itemizing and taking the standard deduction—they apply in addition to either option.

Calculate Your

Paycheck Today!

Calculate your salary paycheks promptly with Paycheck Companion — the freemium paycheck calculator in the market.

Paycheck FAQs

Quick answers to common questions about paychecks and how they work.

Still Have Questions?

Check out our comprehensive blog for in-depth articles on paycheck calculations, tax tips, and financial guidance.

How does a Paycheck Calculator work?

A paycheck calculator estimates your take-home pay by factoring in federal taxes, state taxes, Federal Insurance Contributions Act (FICA) taxes, and deductions from your gross pay.

How are Paychecks useful?

Aside from complying with legal obligations and avoiding fines, paychecks provide employees with the assurance that they’ve been paid correctly. They also help employees and contractors understand their taxes and file their returns.

Is Paycheck Companion really free?

Can I use this for payroll processing?

Our calculator is for estimation purposes. For official payroll processing, please consult a certified payroll professional.